Money Guide | US Fed projections

Money Guide | US Fed projections

Also: Indicators, World Watch, Quick takes, Weekly Agenda, News, Musings, Opportunities

Money Guide is a personal project, supported by paid-subscriptions. I hope that all readers find the news relevant, the musings interesting, the opportunities attractive, and my thoughts enriching

In this issue: China slumping, Mexico rising, Nasdaq rebalancing, PE recovering, Market optimism, USD downturn, and a few thoughts on US Fed projections

*🔒 Forecasts, analysis and additional information locked in the following sections are available only in the premium edition of Money Guide for paid-subscribers

Indicators

The Money Guide Indicators provide you with a macro overview at a glance of financial markets and more detailed information when you zoom-in

Do you want to know more about its components and how are they evaluated?

Part 1: How to read the Indicators from Money Guide

Part 2: Inflation Rates, Central Banks' Rates, Sovereign Bonds, Currency Exchange Rates

Part 3: Commodities, Stocks, Crypto

World Watch

The Money Guide World Watch provides you with a macro overview at a glance of the main situations that can negatively influence economic and financial markets

Do you want to know more?

2023 Threats

2023 Threats’ status updates

My Quick Takes

🔒*** ** ******* **** ****** ********* ****** ******* **** ** **** **** ****. ******* ****** ********* **** ******** ****** ******** ***** ***** **** ** **** ***** *** **** **** ** **** ********, *** ********* ***** ******* ** ******* ** ****** ************.

******* ** * ************ *** ******** * ********* *** ********** *** *** ** **** ** *** ***********, ******, ****** ** * **** **** ** ********* *****, *** * ****** ***** ******. *******, * ************* ********* ***** ** ********* ** *** ** *** ******* ***** ******* **** ***** ***** ******* ******. ******** ********** ***** **** ******* ******** ****** **** ****** ******, ****** * *******, *** *** ** ******* *********** ** ***** **********.

***** ********* *** **** ******* ****. ** ************ ***** ***** *** ***** ** * **** *****, *** ************** ***** *** ****** ******** ****** ** *** *.**** ************** ** ********* **** ****** **** ** *** ***********, ******.

***** ******* ******* *** ******* ***** **** **** ** ***** ******** **** ********** ****** ******, ******** * ***** ******* ***********. ****** *** ** *** ****** ****** ***** ***** ***** **** **** ** *** **** ** *** *** * *** **** ********* ** ** ***** **** *** **** ********* *****. ** ************** ******* ** *** ****** ***** ***** ** *.*** ** ****** ****.

******, *** ***** *** ******** ******** ** ***** ******* ****** ********** ************, **********, **********

****** *** ******* *** ******** *** *********** ******** ** ***** *********.

***** *** **** ******* ******** ** ****** ******* ** *** *** ******* ** ***** ** ***** ******** **** ******** *********** ********.

*********** **** **** ***** **** ** ***** *************** ******, *** ******** ***** ********* **** ****** ** *** ********, ****** ** ******* ******** **** ********* *******.

*** ** ***** ** * **** ******* ** **** **** ** *********.

****** ** ****** ********

*** *****

**** * *********

*** **** ********* ****

*** *** ******* *************🔒

Colored circles in Money Guide refer to estimations of possible economic and financial impact:

🟢=positive mid-term forecast

🔴=negative mid-term forecast

⚪=neutral mid-term forecast

Weekly Agenda

All times are US ET (UTC-4)

Monday, July 24

---

Tuesday, July 25

21:30 🔒 AU Inflation Rate

(Previous: ***, Expected: ***)

Wednesday, July 26

14:00 🔒 US Federal Open Market Committee (FOMC) meeting statements ⚠️

(Previous: ***, Expected: ***)

Thursday, July 27

08:15 🔒 EU ECB Interest Rate decision & statements ⚠️

(Previous: ***, Expected: ***)

23:00 🔒 JP BoJ Interest Rate decision

(Previous: ***, Expected: ***)

Friday, July 28

08:30 🔒 US Personal Consumption and Expenditures (PCE) Index report ⚠️

(Previous: ***, Expected: ***)

Q2 Earnings reports during the week

⚠️Probable high volatility when information is released to the public

(Click here to read about the usual market behavior)

Take advantage of this limited-time offer:

News

📰 🟢 What’s behind the Stock market rally (it’s not just Big Tech) | Many companies are adding to the S&P 500’s rise after Microsoft, Apple, Nvidia and others led the charge this spring. The breadth signals stocks could keep climbing (link)

📰 ⚪ What is Nasdaq's special rebalancing and its impact? | A "special rebalance" of the Nasdaq 100 index will take place later this month as exchange operator Nasdaq looks to reduce the concentration of heavyweight companies that account for nearly half of the index's weight (link)

📰 🔴 China addresses investor concerns in meeting with global funds | Chinese regulators met with global investors, stepping up the government’s bid to boost market confidence as the country’s economic recovery loses steam (link)

📰 🟢 Private company valuations show signs of recovery | Private company stocks are now trading at levels that are close to the valuations achieved during their second-most recent funding rounds (link)

Fractionalized car trading startup Rally settles with SEC | The Securities and Exchange Commission settled charges that Rally, a fractionalized car and memorabilia investment startup, had been operating as an unregistered exchange (link)

📰 ⚪ Bluechip | Bluechip is an independent nonprofit stablecoin rating agency (link)

Musings

💭 🟢 Is the Yield Curve a Reliable Recession Signal Anymore? | We’re right in the time period after a yield curve inversion that one should expect a recession. But doubts are now cropping up about the reliability of the curve as a predictor of the business cycle (link)

💭 🟢 Markets appear convinced the US Fed can pull off a soft landing | Stocks surged on evidence that inflation is cooling (link)

💭 🟢 Pimco’s Clarida says market bets on US march rate cut make sense | Former Federal Reserve Vice Chairman Richard Clarida said market wagers on US interest-rate cuts in March are understandable given a scenario where there’s a “softish landing” and the central bank is confident it’s reined in inflation (link)

Opportunities

💡 US Dollar’s busted bull run has bears calling end of an era | It’s hard to overstate the potential ripple effects from a long-term greenback slide. It would reduce import prices for developing nations, bolster currencies, boost American firms’ exports at the expense of their counterparts in Europe, Asia and elsewhere (link)

💡 The US is short on homes. Here's how builders are still offering the American dream | America is in the middle of a housing crisis. There are only 1.08 million existing homes on the market, and the affordability of a single-family home is at its lowest level in several decades. One bid to close the estimated 3.8 million unit deficit in housing is by building new, single-family homes, but some are not for sale, they’re for rent (link)

💡 Mexico surpassed China as the top U.S. trading partner | The decline of China as the country's top trading partner comes after years of worsening US-China relations and reflects Mexico's rise in manufacturing -hastened along by a new push to "nearshore" that work closer to the US (link)

A few thoughts on…

US Fed projections

The US Fed has a double mandate: price stability and full employment (see Jobs & inflation). To achieve that, they ease or tighten economic conditions. In general terms, price stability requires tighter conditions, and full employment requires easier conditions.

Currently, the Fed is not very worried about rising unemployment levels, since they are at historic lows, they are more focused on inflation, hoping to reach a 2% annual average inflation rate.

The main tool the US Fed can use to tighten economic conditions is the “Federal Funds Target Rate”, the rate at which banks lend money to each other. All other rates are dependent on that one, because each step adds additional interest until it gets to mortgages, credit card rates, commercial loans, etcetera

By raising rates, money becomes more expensive to borrow, and interest makes future money more valuable. The overall result is a reduction on the general economic activity, and the market forces that normally push prices higher (investing, development and supply/demand dynamics) (see Interpreting the Indicators [part 2]).

Usually, economic tightening can lead to recessions, but right now the US economy seems strong: unemployment is low, consumption is high, inflation is easing, stock valuations are trending upwards, investors are expecting target-interest-rates cuts.

As we have said, the Fed is pushing towards a 2% YoY inflation rate for the long term. The origin of that 2% number is arbitrary, but it has entrenched itself in Central Banks’ mindsets: inflation is desirable, but high inflation is not, so 1% annually seemed like a good target, and by adding some tolerance it became 2%.

Most of the times, it’s important to evaluate Year-on-Year (YoY) rates alongside Month-on-Month (MoM) rates for a more complete picture. A 2% Year-on-Year (YoY) inflation rate is close to 0.165% Month-on-Month (MoM) inflation rate.

Where are we now?

According to the latest US Consumer Price Index (CPI) report, Month-on-Month inflation has decreased dramatically since last year. Accordingly, YoY inflation has come down from near 10% to almost 3%, and the current 12-month average of MoM inflation is 0.25%

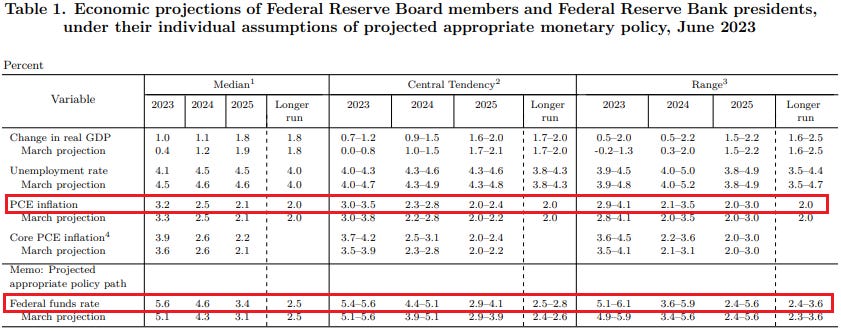

What is the US Fed expecting?

At regular intervals, the Federal Open Market Committee releases a “Summary of Economic Projections”. The most recent one includes this table:

Inflation rates are expected to continue trending down, with inflation hovering around 2.50% YoY during 2024, and close to 2.00% on 2025.

Federal Funds Target rates are expected to peak this year near 5.50%, and slowly decrease to 2.50% for the long-term.

We can group those projections and previous inflation reports in a single graph:

The graph makes clear that the US Fed believes the fight against inflation is not over. By keeping a significant spread between interest rates and inflation rates, they are trying to limit economic growth and avoid renewed inflationary pressures. Also, a large spread gives them more flexibility to ease or tighten conditions as they see fit. Maybe they will be able to tame inflation and avoid a recession at the same time. This week’s FOMC press conference should be closely watched for messages that confirm or challenge these projections.

take care, have fun, be chill

-SM

Enjoyed the content?

Subscribe to Money Guide to receive every new edition of The Chosen Many newsletters directly in your inbox, get instant access to all the archives and resources at our website, and join our private channel for additional up-to-date content.

Never miss an update and be a part of the conversation…

There is more to life than money. Be in the know…

twitter: @TheChosenMany

threads: @TheChosenMany_bySM

Spread the word